Cell and Gene therapy (CGT) pipeline deep dive

NEWDIGS FoCUS has conducted a unique, detailed, indication-by-indication analysis to estimate the expected volume of durable cell and gene therapies (CGT) likely to be available on the US market in the coming years. FoCUS has maintained its Pipeline Analysis and Modeling (PAM) initiative in order to inform stakeholder decision-making for sustainable, appropriate patient access to CGTs.

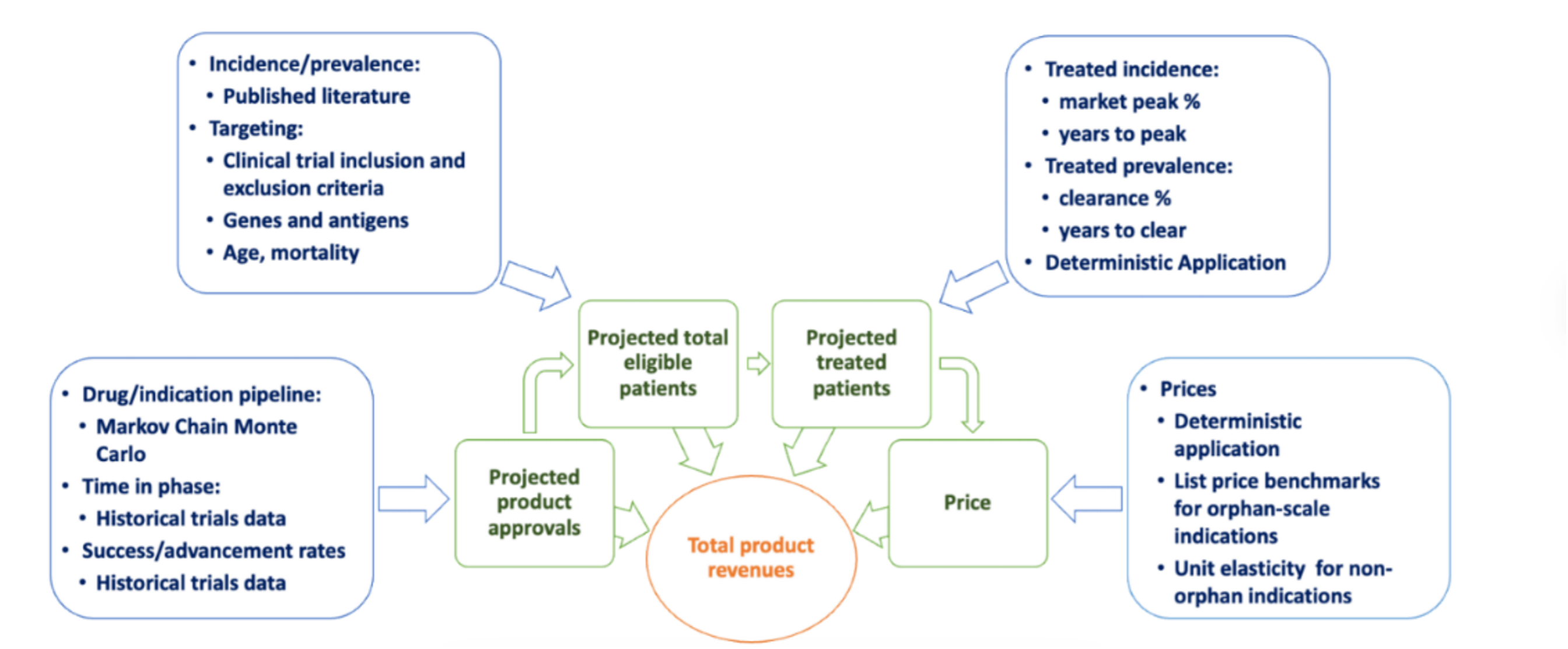

Figure 1 Overview of inputs to pipeline analysis

Through PAM, FoCUS assesses and revises over time detailed estimates of clinical trial progression rates, disease incidence and prevalence, and estimated patient uptake for each product-indication (defined as the disease indication matched to the product and its target gene or antigen; a single product could have multiple product-indications). Figure 1 depicts a synthesis of the approach to develop all estimates. Details on the data synthesis may be found here.

Updated results are published periodically. The most recent publication, Pediatric-onset rare disease therapy pipeline yields hope for some and gaps for many: 10-year projection of approvals, treated patients, and list price revenues provided pediatric specific projections for therapy approvals. The results of the 2024 pipeline analysis are soon to be published. Pipeline data through December 2023 are found below.

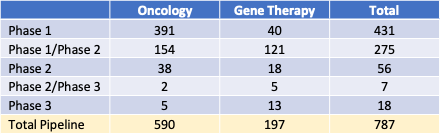

Table 1: Pipeline Products by development phase, 2023

Table 1 lists numbers of products in clinical trials as oncology or gene therapy products. Approximately 75% of the product candidates in development beyond the pre-clinical phase are for oncology patients, 168 (21%) are for orphan, non-oncology indications, and 29 (4%) are to treat larger therapeutic areas such as cardiovascular conditions.

The current pipeline of US-targeted therapies is expected to result in 85 product-indication approvals (estimated range 75–96) by 2033. Considering the existing 21 unique products with 34 product indication approvals and an average of four to eight new approvals annually for the next ten years, an estimated 85 conditions will be treated with cell and gene therapies by 2033.

This estimate reflects the current pipeline. The pipeline will, however, continue to be updated with new innovations. Thus, towards the back end of this timeframe, we may see additional products launch beyond those reflected here.

Expected patient volume

Estimates for the number of patients to be treated each year are generated from the products in the pipeline and their projected approval dates. FoCUS manually determined estimates of treatment-eligible incident and prevalent patient populations using a range of sources that varied by disease.

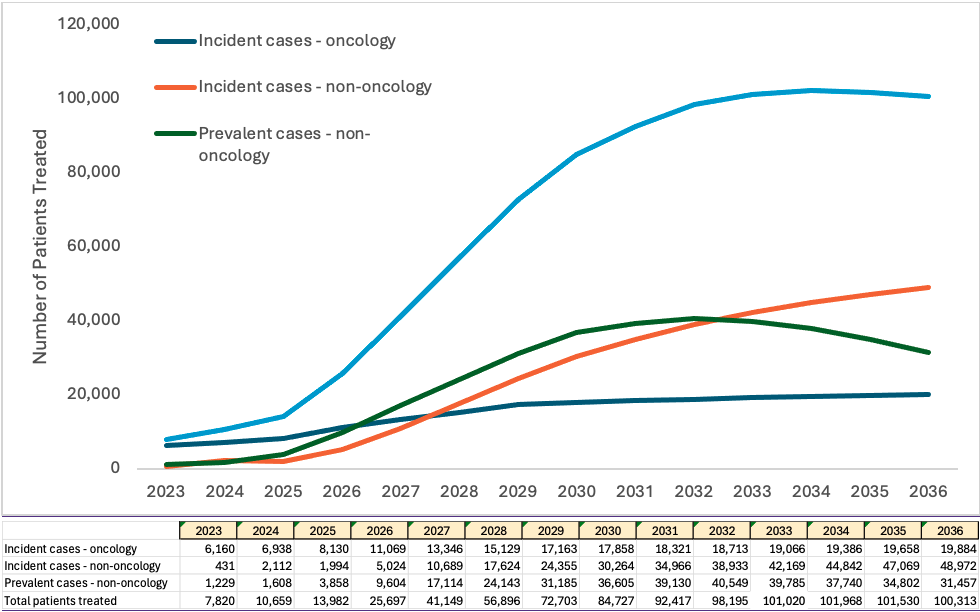

The incident population refers to the number of new cases of a characteristic or condition that develop in a specified time period. The prevalent population refers to those who have a specific characteristic or condition in a given time period, and are already living with the disease or condition, such as hemophilia or sickle cell disease. Our analysis determined that the treatment of the prevalent population will peak in 2031 and 2032, and then will decline as numbers of untreated patients decline.

Based on estimated prevalence and incidence and adoption rate assumptions, by 2032, the treatable patient population for CGT is anticipated to be 105,000+ patients per year.

Figure 2: Projection of treated patients per year

Figure 2: Projection of treated patients per year

The key uncertainty within the FoCUS model lies in the market penetration and adoption rate for these new-to-world therapies. The model makes assumptions about two parameters for each disease’s incidence and prevalence:

- Peak market penetration: What percentage of the clinically-eligible population will be treated?

- Time to peak/adoption rate: How long to achieve the peak? (from 1 to 7 years)

Market Penetration refers to the number of individuals likely to be treated, divided by the number of treatment-eligible individuals. In practice, the ‘likely to be treated’ population is expected to be smaller than the 'treatable’ population.

For diseases with severe consequences, the likely treated/treatable percentage is anticipated to be high, subject to any challenges in identifying appropriate patients. For diseases with less severe or more long-term consequences, only a small percentage of eligible patients may be treated. Using an appropriate modifier is vital for any analysis, as the total eligible population may substantially overestimate the number of patients treated.

There is no simple way to anticipate an appropriate market penetration percentage, unfortunately, as market penetration is influenced by multiple factors that will vary in significance by disease. The PAM analysis includes disease-specific factors that will influence market penetration.

- Age at onset: is the diagnosis in infancy, nearing the end of life, or in between?

- Impact on life expectancy: can an individual live with the disease or is life expectancy greatly shortened?

- Therapeutic options: are there alternative treatments? Are they sufficiently effective?

- Therapeutic costs: will the overall cost of care be lessened by the new treatment?

- Symptoms: how do the symptoms impact the quality of life for the patient? What is the impact on the patient’s family as caregivers, if any?

The product uptake or adoption rate reflects how quickly patients likely to be treated will receive treatment. Market conditions that may impact the speed of uptake include payer coverage decisions, provider availability, local market access, etc. Treatment adoption may also differ for newly diagnosed patients compared to a population pool living with the disease. Diseases with high mortality rates would likely be associated with high adoption. Patients with diseases that have existing therapies may choose a ‘wait and see’ approach to treatment, slowing adoption.

Broadly, the pipeline analysis assumed that conditions with limited treatment alternatives and more severe or fatal consequences will see greater and faster adoption. FoCUS will continue to explore the influence of disease severity as greater real-world data is produced on patient and physician treatment choices.

The PAM team completed a comparison in October 2023 of the clinical trail success rates and overall likelihood of approval from the PAM model to other recently published estimates of success rates from all therapeutic modalities. The research suggests that durable CGT programs have higher success once they enter the clinic compared to the combined pipelin of all therapies. You can read more in the research brief Are Cell and Gene Therapy programs a better bet?